25 minutes

Written: 2020-02-18 22:00 +0000

ISLR :: Resampling Methods

Chapter V - Resampling Methods

All the questions are as per the ISL seventh printing of the First edition1.

Common

Instead of using the standard functions, we will leverage the mlr3

package2.

1#install.packages("mlr3","data.table","mlr3viz","mlr3learners")

Actually for R version 3.6.2, the steps to get it working were a bit

more involved.

1install.packages("remotes","data.table",

2 "GGally","precerec") # For plots

1library(remotes)

2remotes::install_github("mlr-org/mlr3")

3remotes::install_github("mlr-org/mlr3viz")

4remotes::install_github("mlr-org/mlr3learners")

Load ISLR and other libraries.

1libsUsed<-c("dplyr","ggplot2","tidyverse",

2 "ISLR","caret","MASS",

3 "pROC","mlr3","data.table",

4 "mlr3viz","mlr3learners")

5invisible(lapply(libsUsed, library, character.only = TRUE))

Question 5.5 - Page 198

In Chapter 4, we used logistic regression to predict the probability of

default using income and balance on the Default data set. We

will now estimate the test error of this logistic regression model using

the validation set approach. Do not forget to set a random seed before

beginning your analysis.

(a) Fit a logistic regression model that uses income and balance to

predict default.

(b) Using the validation set approach, estimate the test error of this model. In order to do this, you must perform the following steps:

Split the sample set into a training set and a validation set.

Fit a multiple logistic regression model using only the training observations.

Obtain a prediction of default status for each individual in the validation set by computing the posterior probability of default for that individual, and classifying the individual to the

defaultcategory if the posterior probability is greater than \(0.5\).Compute the validation set error, which is the fraction of the observations in the validation set that are misclassified.

(c) Repeat the process in (b) three times, using three different splits of the observations into a training set and a validation set. Comment on the results obtained.

(d) Now consider a logistic regression model that predicts the prob-

ability of default using income , balance , and a dummy variable

for student. Estimate the test error for this model using the

validation set approach. Comment on whether or not including a dummy

variable for student leads to a reduction in the test error rate.

Answer

We will need our data.

1defDat<-ISLR::Default

- Very quick peek

1defDat %>% summary

1## default student balance income

2## No :9667 No :7056 Min. : 0.0 Min. : 772

3## Yes: 333 Yes:2944 1st Qu.: 481.7 1st Qu.:21340

4## Median : 823.6 Median :34553

5## Mean : 835.4 Mean :33517

6## 3rd Qu.:1166.3 3rd Qu.:43808

7## Max. :2654.3 Max. :73554

1defDat %>% str

1## 'data.frame': 10000 obs. of 4 variables:

2## $ default: Factor w/ 2 levels "No","Yes": 1 1 1 1 1 1 1 1 1 1 ...

3## $ student: Factor w/ 2 levels "No","Yes": 1 2 1 1 1 2 1 2 1 1 ...

4## $ balance: num 730 817 1074 529 786 ...

5## $ income : num 44362 12106 31767 35704 38463 ...

a) Logistic Model with mlr3

Following the new approach which leverages R6 features leads us to define a classification task first. As far as I can tell, the data needs to be filtered to contain only the things we need to predict with, in this case we are required to use only income and balance so we will do so.

1set.seed(1984)

2redDat<-defDat %>% subset(select=c(income,balance,default))

3tskLogiFull=TaskClassif$new(id="credit",backend=redDat,target="default")

4print(tskLogiFull)

1## <TaskClassif:credit> (10000 x 3)

2## * Target: default

3## * Properties: twoclass

4## * Features (2):

5## - dbl (2): balance, income

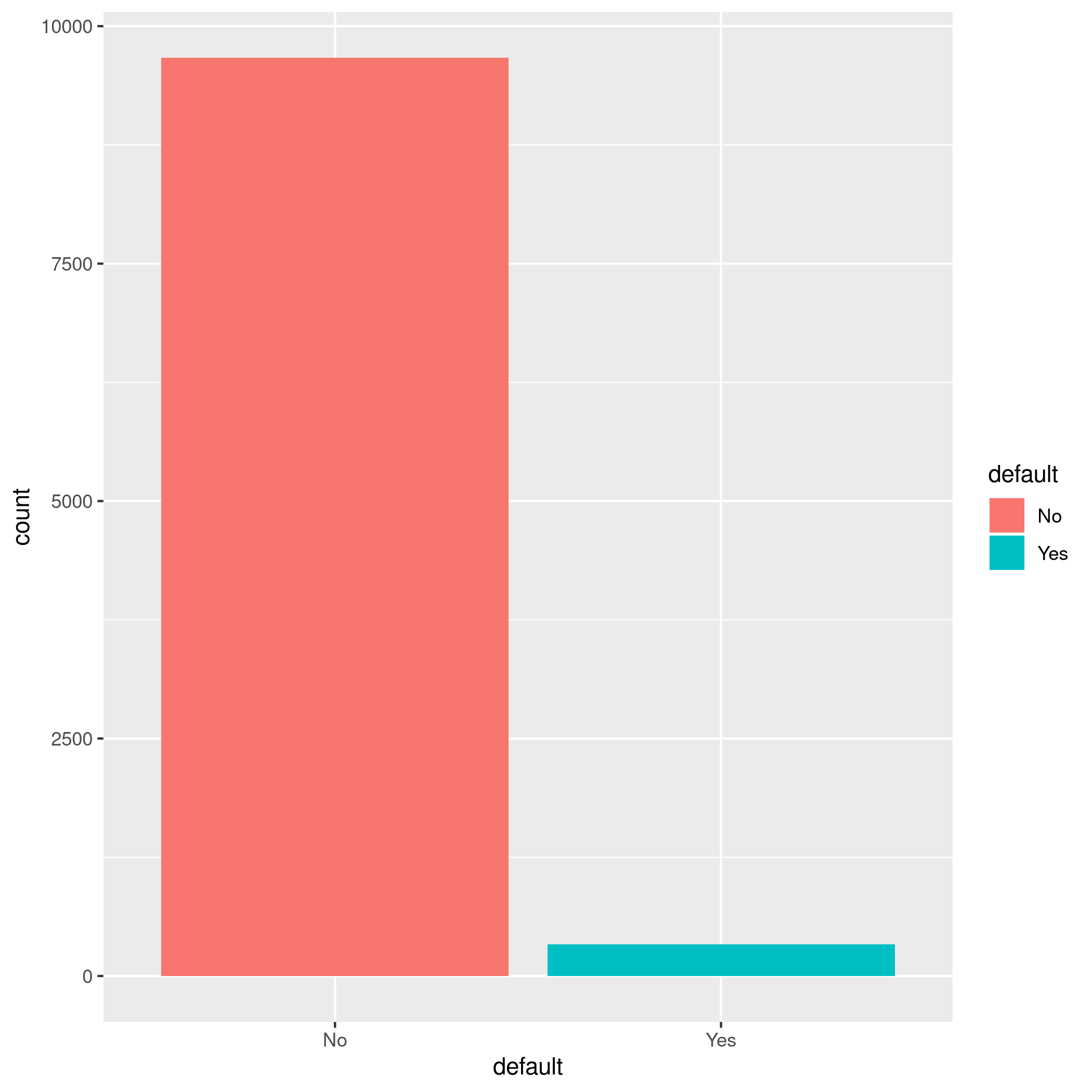

This can be visualized neatly as well.

1autoplot(tskLogiFull)

Figure 1: MLR3 Visualizations

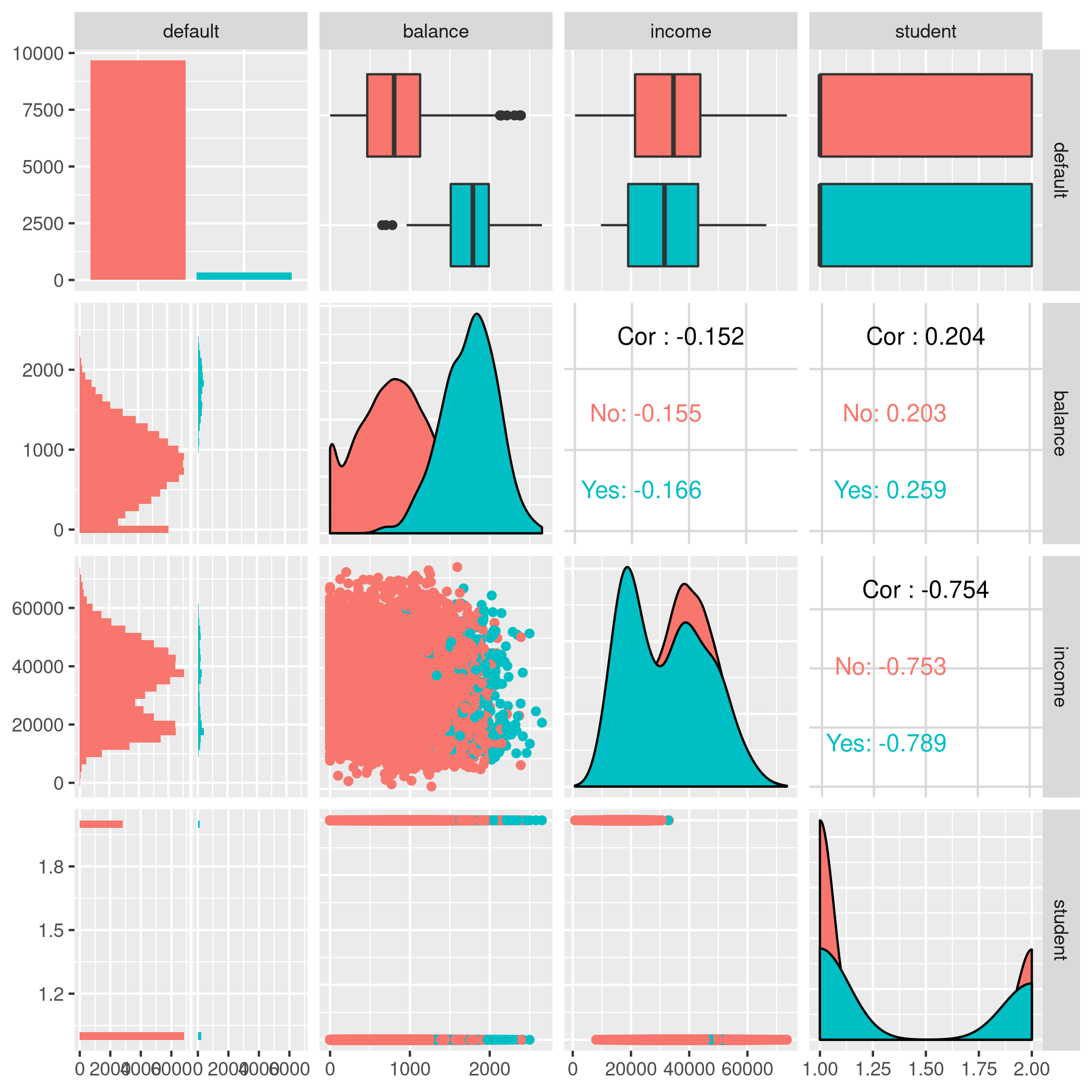

We have a pretty imbalanced data-set.

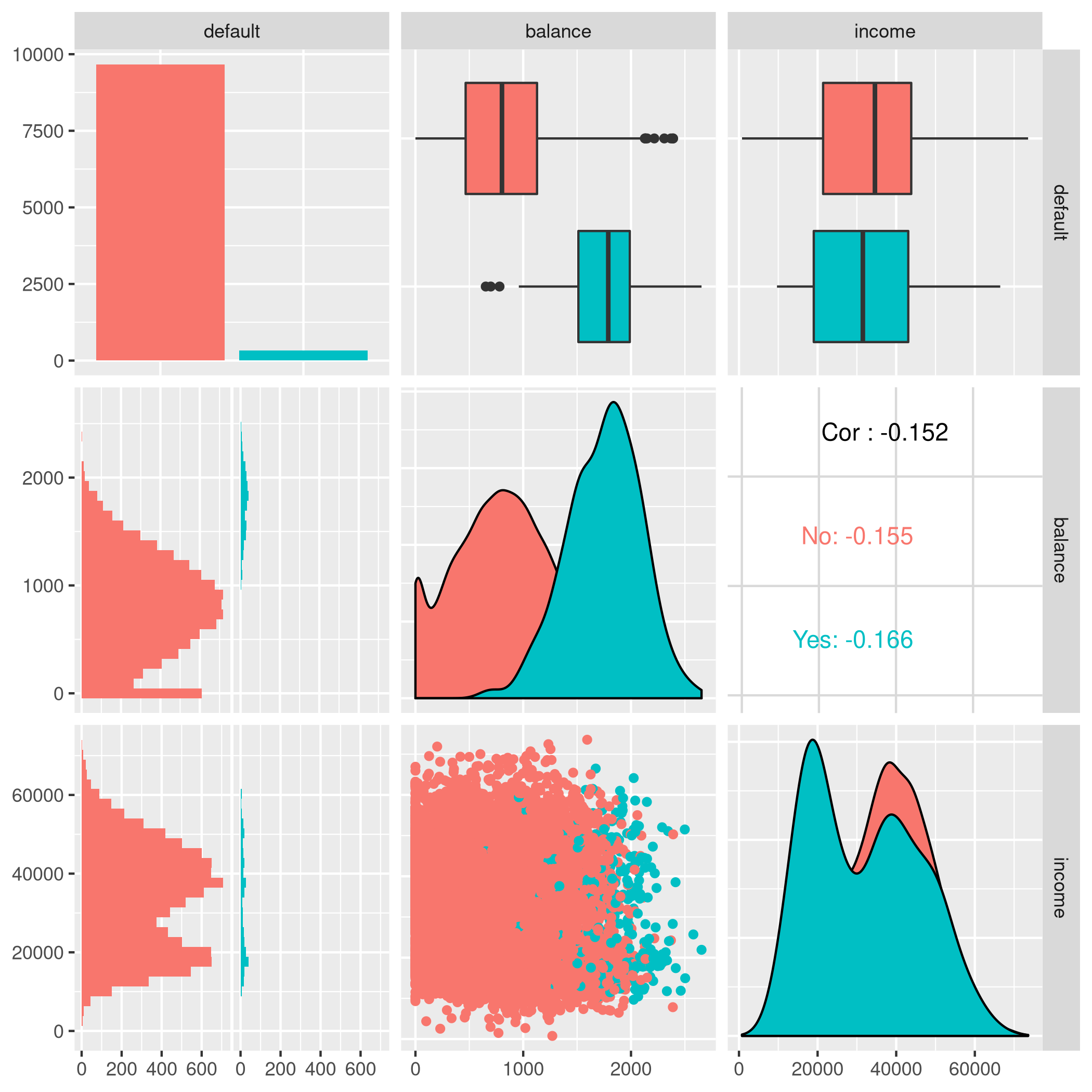

1autoplot(tskLogiFull,type="pairs")

1## Registered S3 method overwritten by 'GGally':

2## method from

3## +.gg ggplot2

1## `stat_bin()` using `bins = 30`. Pick better value with `binwidth`.

2## `stat_bin()` using `bins = 30`. Pick better value with `binwidth`.

Figure 2: Paired mlr3 data

We can use any of the learners implemented, so it is a good idea to take a quick peek at them all.

1as.data.table(mlr_learners)

1## key feature_types

2## 1: classif.debug logical,integer,numeric,character,factor,ordered

3## 2: classif.featureless logical,integer,numeric,character,factor,ordered

4## 3: classif.glmnet logical,integer,numeric

5## 4: classif.kknn logical,integer,numeric,factor,ordered

6## 5: classif.lda logical,integer,numeric,factor,ordered

7## 6: classif.log_reg logical,integer,numeric,character,factor,ordered

8## 7: classif.naive_bayes logical,integer,numeric,factor

9## 8: classif.qda logical,integer,numeric,factor,ordered

10## 9: classif.ranger logical,integer,numeric,character,factor,ordered

11## 10: classif.rpart logical,integer,numeric,factor,ordered

12## 11: classif.svm logical,integer,numeric

13## 12: classif.xgboost logical,integer,numeric

14## 13: regr.featureless logical,integer,numeric,character,factor,ordered

15## 14: regr.glmnet logical,integer,numeric

16## 15: regr.kknn logical,integer,numeric,factor,ordered

17## 16: regr.km logical,integer,numeric

18## 17: regr.lm logical,integer,numeric,factor

19## 18: regr.ranger logical,integer,numeric,character,factor,ordered

20## 19: regr.rpart logical,integer,numeric,factor,ordered

21## 20: regr.svm logical,integer,numeric

22## 21: regr.xgboost logical,integer,numeric

23## key feature_types

24## packages

25## 1:

26## 2:

27## 3: glmnet

28## 4: kknn

29## 5: MASS

30## 6: stats

31## 7: e1071

32## 8: MASS

33## 9: ranger

34## 10: rpart

35## 11: e1071

36## 12: xgboost

37## 13: stats

38## 14: glmnet

39## 15: kknn

40## 16: DiceKriging

41## 17: stats

42## 18: ranger

43## 19: rpart

44## 20: e1071

45## 21: xgboost

46## packages

47## properties

48## 1: missings,multiclass,twoclass

49## 2: importance,missings,multiclass,selected_features,twoclass

50## 3: multiclass,twoclass,weights

51## 4: multiclass,twoclass

52## 5: multiclass,twoclass,weights

53## 6: twoclass,weights

54## 7: multiclass,twoclass

55## 8: multiclass,twoclass,weights

56## 9: importance,multiclass,oob_error,twoclass,weights

57## 10: importance,missings,multiclass,selected_features,twoclass,weights

58## 11: multiclass,twoclass

59## 12: importance,missings,multiclass,twoclass,weights

60## 13: importance,missings,selected_features

61## 14: weights

62## 15:

63## 16:

64## 17: weights

65## 18: importance,oob_error,weights

66## 19: importance,missings,selected_features,weights

67## 20:

68## 21: importance,missings,weights

69## properties

70## predict_types

71## 1: response,prob

72## 2: response,prob

73## 3: response,prob

74## 4: response,prob

75## 5: response,prob

76## 6: response,prob

77## 7: response,prob

78## 8: response,prob

79## 9: response,prob

80## 10: response,prob

81## 11: response,prob

82## 12: response,prob

83## 13: response,se

84## 14: response

85## 15: response

86## 16: response,se

87## 17: response,se

88## 18: response,se

89## 19: response

90## 20: response

91## 21: response

92## predict_types

We can now pick the logistic one.

Note that this essentially

proxies our requests down to the stats package.

1learner = mlr_learners$get("classif.log_reg")

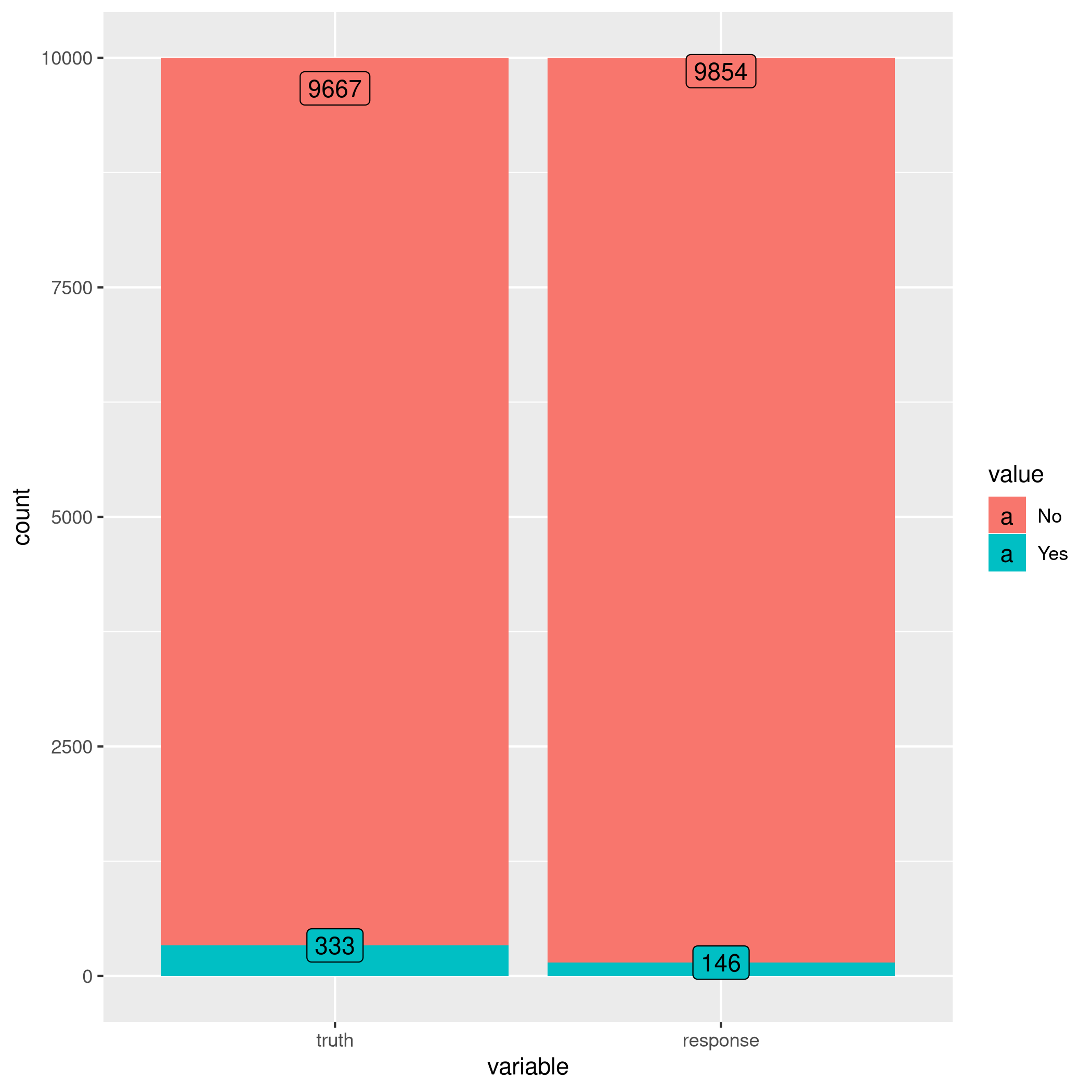

Now we can final solve the question, which is to simply use the model on all our data and return the accuracy metrics.

1trainFullCred=learner$train(tskLogiFull)

2print(learner$predict(tskLogiFull)$confusion)

1## truth

2## response No Yes

3## No 9629 225

4## Yes 38 108

1measure = msr("classif.acc")

2print(learner$predict(tskLogiFull)$score(measure))

1## classif.acc

2## 0.9737

Note that this style of working with objects does not really utilize the

familiar %>% interface.

The caret package still has neater default metrics so we will use that

as well.

1confusionMatrix(learner$predict(tskLogiFull)$response,defDat$default)

1## Confusion Matrix and Statistics

2##

3## Reference

4## Prediction No Yes

5## No 9629 225

6## Yes 38 108

7##

8## Accuracy : 0.9737

9## 95% CI : (0.9704, 0.9767)

10## No Information Rate : 0.9667

11## P-Value [Acc > NIR] : 3.067e-05

12##

13## Kappa : 0.4396

14##

15## Mcnemar's Test P-Value : < 2.2e-16

16##

17## Sensitivity : 0.9961

18## Specificity : 0.3243

19## Pos Pred Value : 0.9772

20## Neg Pred Value : 0.7397

21## Prevalence : 0.9667

22## Detection Rate : 0.9629

23## Detection Prevalence : 0.9854

24## Balanced Accuracy : 0.6602

25##

26## 'Positive' Class : No

27##

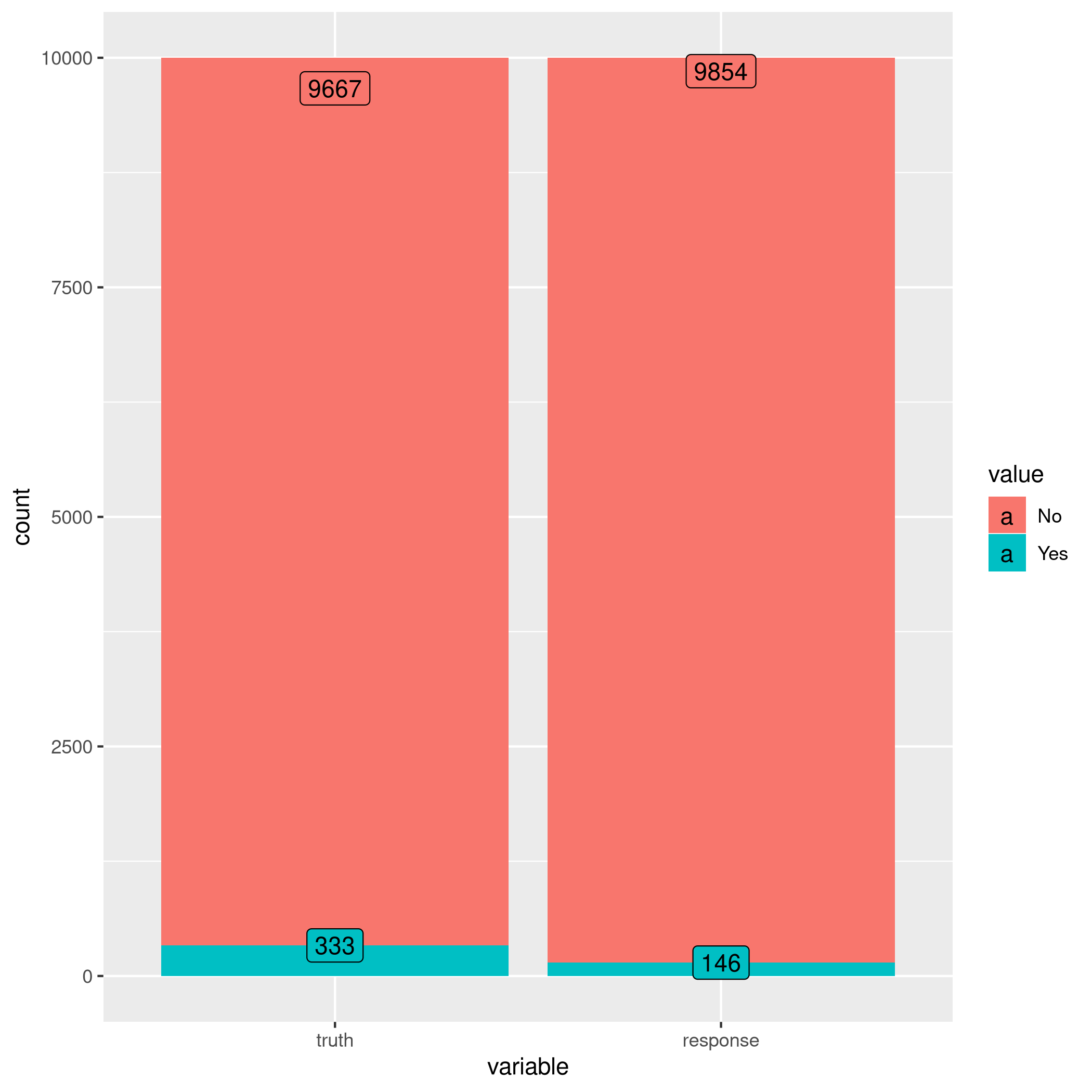

1autoplot(learner$predict(tskLogiFull))

Figure 3: Autoplot results

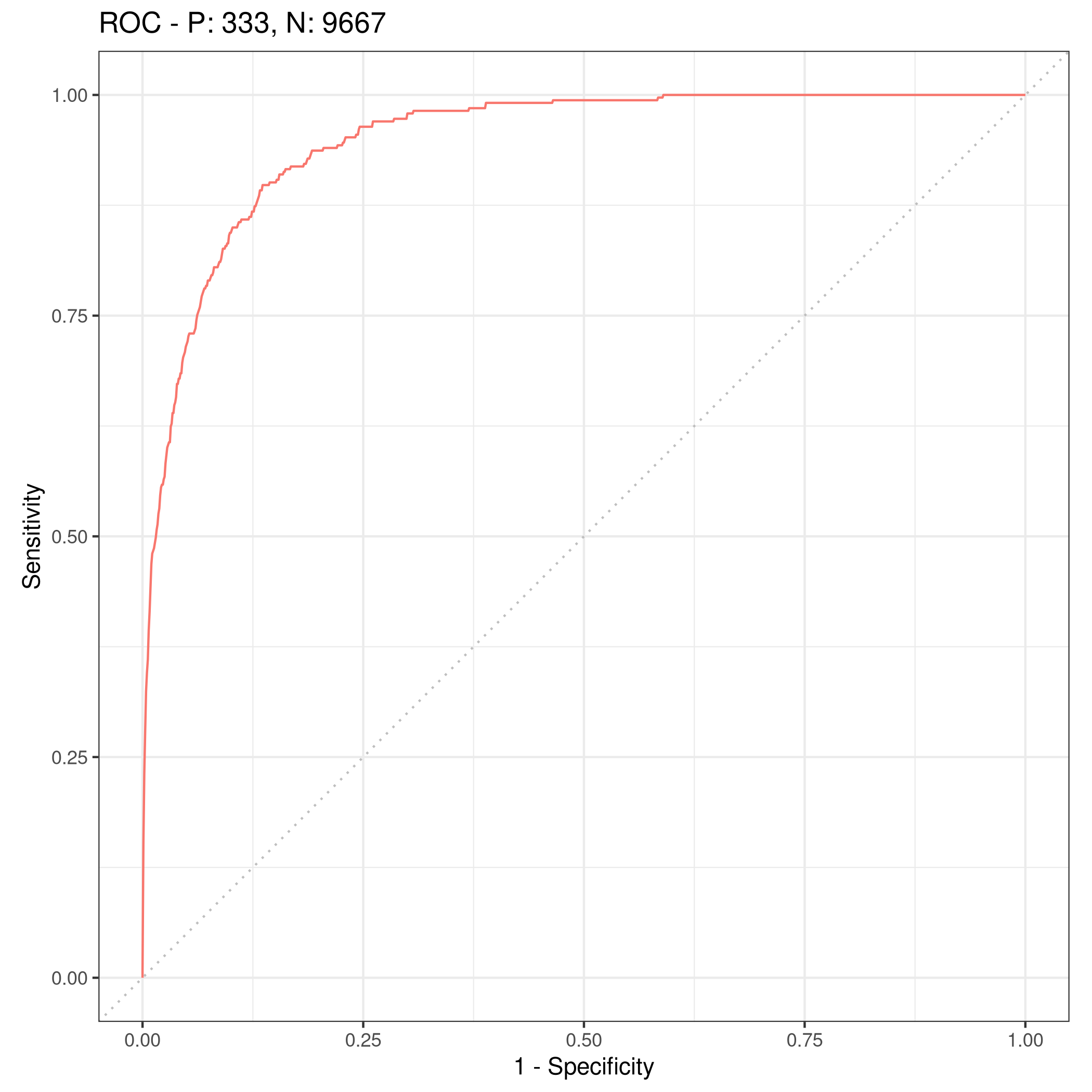

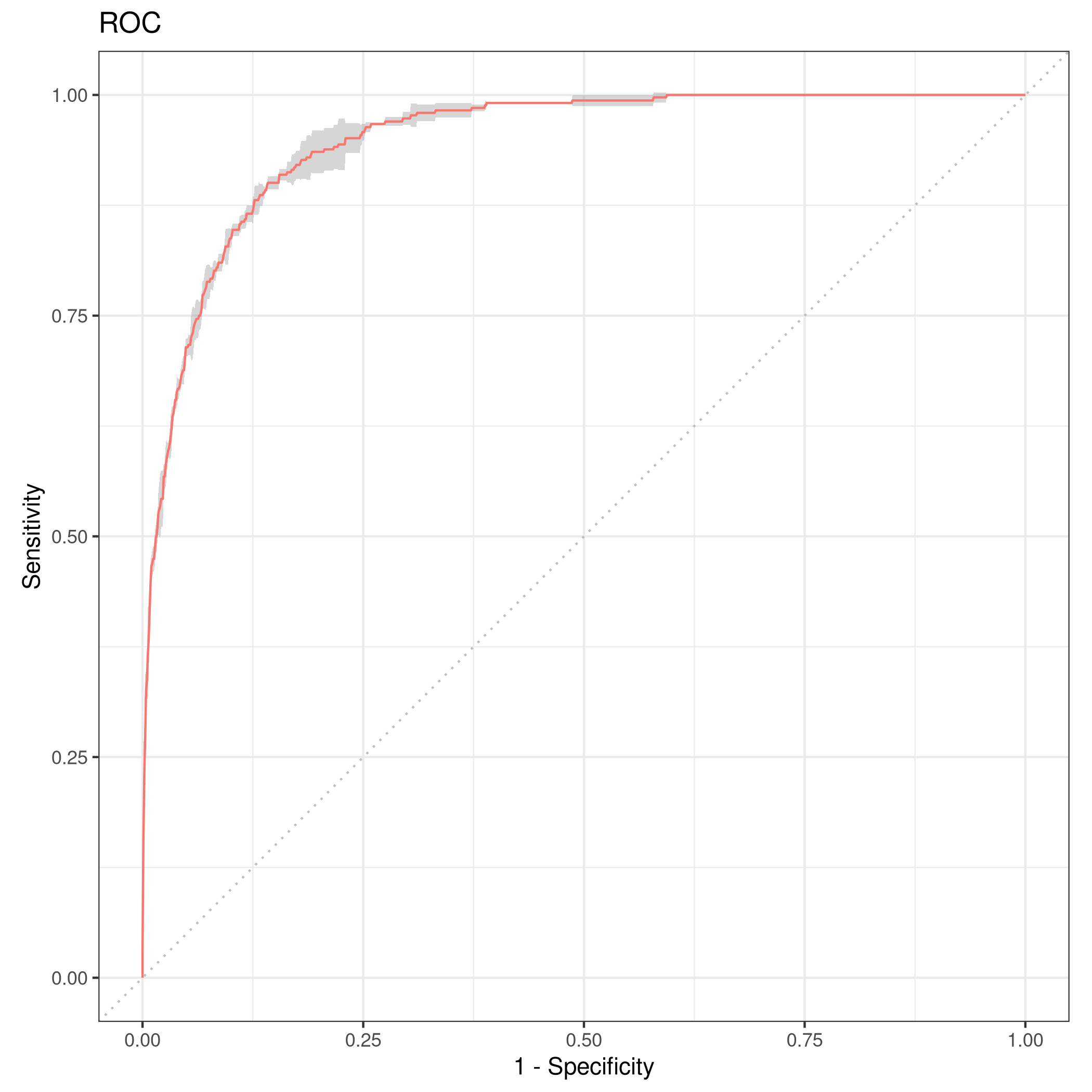

We can get some other plots as well, but we need our probabilities to be returned.

1# For ROC curves

2lrnprob = lrn("classif.log_reg",predict_type="prob")

3lrnprob$train(tskLogiFull)

4autoplot(lrnprob$predict(tskLogiFull),type="roc")

Figure 4: ROC curve

b) Validation Sets with mlr3

Though the question seems to require a manual validation set generation and thresholding, we can simply use the defaults.

1train_set = sample(tskLogiFull$nrow, 0.8 * tskLogiFull$nrow)

2test_set = setdiff(seq_len(tskLogiFull$nrow), train_set)

3learner$train(tskLogiFull,row_ids=train_set)

4confusionMatrix(learner$predict(tskLogiFull, row_ids=test_set)$response,defDat[-train_set,]$default)

1## Confusion Matrix and Statistics

2##

3## Reference

4## Prediction No Yes

5## No 1921 47

6## Yes 9 23

7##

8## Accuracy : 0.972

9## 95% CI : (0.9638, 0.9788)

10## No Information Rate : 0.965

11## P-Value [Acc > NIR] : 0.04663

12##

13## Kappa : 0.4387

14##

15## Mcnemar's Test P-Value : 7.641e-07

16##

17## Sensitivity : 0.9953

18## Specificity : 0.3286

19## Pos Pred Value : 0.9761

20## Neg Pred Value : 0.7188

21## Prevalence : 0.9650

22## Detection Rate : 0.9605

23## Detection Prevalence : 0.9840

24## Balanced Accuracy : 0.6620

25##

26## 'Positive' Class : No

27##

For a reasonable comparison, we will demonstrate a standard approach as

well. In this instance we will not use caret to ensure that our class

distribution in the train and test sets are not sampled to remain the

same.

1trainNoCaret<-sample(nrow(defDat), size = floor(.8*nrow(defDat)), replace = F)

2glm.fit=glm(default~income+balance,data=defDat,family=binomial,subset=trainNoCaret)

3glm.probs<-predict(glm.fit,defDat[-trainNoCaret,],type="response")

4glm.preds<-ifelse(glm.probs < 0.5, "No", "Yes")

5confusionMatrix(glm.preds %>% factor,defDat[-trainNoCaret,]$default)

1## Confusion Matrix and Statistics

2##

3## Reference

4## Prediction No Yes

5## No 1930 46

6## Yes 6 18

7##

8## Accuracy : 0.974

9## 95% CI : (0.966, 0.9805)

10## No Information Rate : 0.968

11## P-Value [Acc > NIR] : 0.06859

12##

13## Kappa : 0.3986

14##

15## Mcnemar's Test P-Value : 6.362e-08

16##

17## Sensitivity : 0.9969

18## Specificity : 0.2812

19## Pos Pred Value : 0.9767

20## Neg Pred Value : 0.7500

21## Prevalence : 0.9680

22## Detection Rate : 0.9650

23## Detection Prevalence : 0.9880

24## Balanced Accuracy : 0.6391

25##

26## 'Positive' Class : No

27##

Since the two approaches use different samples there is a little variation, but we can see that the accuracy is essentially the same.

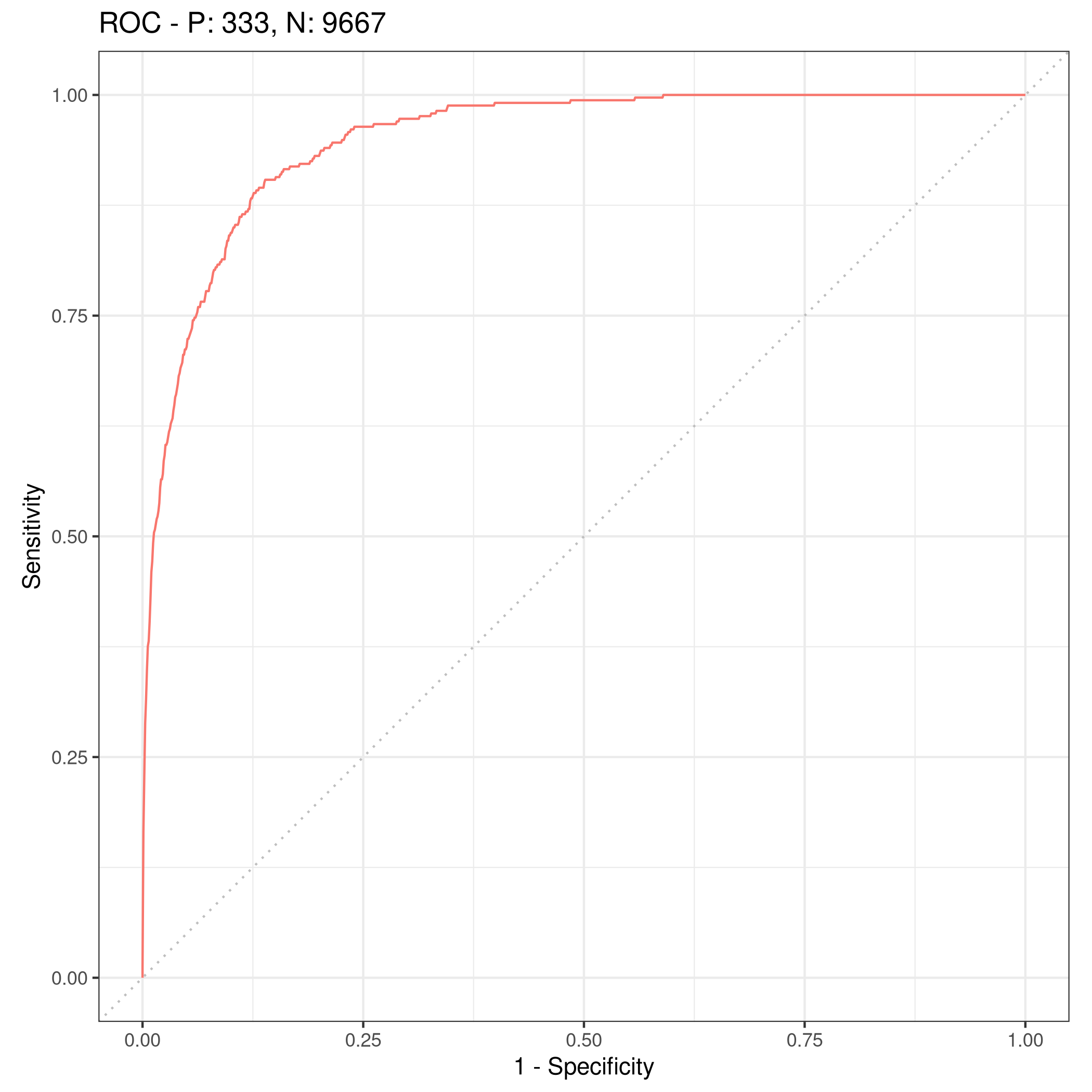

c) 3-fold cross validation

As per the question, we can repeat the block above three times, or

extract it into a function which takes a seed value and run that three

times. Either way, here we will present the mlr3 approach to cross

validation and resampling.

1rr = resample(tskLogiFull, lrnprob, rsmp("cv", folds = 3))

1## INFO [22:12:30.025] Applying learner 'classif.log_reg' on task 'credit' (iter 1/3)

2## INFO [22:12:30.212] Applying learner 'classif.log_reg' on task 'credit' (iter 2/3)

3## INFO [22:12:30.360] Applying learner 'classif.log_reg' on task 'credit' (iter 3/3)

1autoplot(rr,type="roc")

Figure 5: Resampled ROC curve

We might want the average as well.

1rr$aggregate(msr("classif.ce")) %>% print

1## classif.ce

2## 0.02630035

Adding Student as a dummy variable

We will stick to the mlr3 approach because it is faster.

1redDat2<-defDat %>% mutate(student=as.numeric(defDat$student))

2tskLogi2=TaskClassif$new(id="credit",backend=redDat2,target="default")

3print(tskLogi2)

1## <TaskClassif:credit> (10000 x 4)

2## * Target: default

3## * Properties: twoclass

4## * Features (3):

5## - dbl (3): balance, income, student

1autoplot(tskLogi2,type="pairs")

1## `stat_bin()` using `bins = 30`. Pick better value with `binwidth`.

2## `stat_bin()` using `bins = 30`. Pick better value with `binwidth`.

3## `stat_bin()` using `bins = 30`. Pick better value with `binwidth`.

Figure 6: Logistic regression pairs data

This gives us a visual indicator and premonition that we might not be getting incredible results with our new variable in the mix, but we should still work it through.

1confusionMatrix(lrnprob$predict(tskLogi2)$response,defDat$default)

1## Confusion Matrix and Statistics

2##

3## Reference

4## Prediction No Yes

5## No 9629 225

6## Yes 38 108

7##

8## Accuracy : 0.9737

9## 95% CI : (0.9704, 0.9767)

10## No Information Rate : 0.9667

11## P-Value [Acc > NIR] : 3.067e-05

12##

13## Kappa : 0.4396

14##

15## Mcnemar's Test P-Value : < 2.2e-16

16##

17## Sensitivity : 0.9961

18## Specificity : 0.3243

19## Pos Pred Value : 0.9772

20## Neg Pred Value : 0.7397

21## Prevalence : 0.9667

22## Detection Rate : 0.9629

23## Detection Prevalence : 0.9854

24## Balanced Accuracy : 0.6602

25##

26## 'Positive' Class : No

27##

1autoplot(lrnprob$predict(tskLogi2))

Figure 7: Autoplot figure

1lrnprob$train(tskLogi2)

2autoplot(lrnprob$predict(tskLogi2),type="roc")

Figure 8: ROC plot

Although we have slightly better accuracy with the new variable, it needs to be compared to determine if it is worth further investigation.

With a three-fold validation approach,

1library("gridExtra")

1##

2## Attaching package: 'gridExtra'

1## The following object is masked from 'package:dplyr':

2##

3## combine

1rr2 = resample(tskLogi2, lrnprob, rsmp("cv", folds = 3))

1## INFO [22:12:39.670] Applying learner 'classif.log_reg' on task 'credit' (iter 1/3)

2## INFO [22:12:39.731] Applying learner 'classif.log_reg' on task 'credit' (iter 2/3)

3## INFO [22:12:39.780] Applying learner 'classif.log_reg' on task 'credit' (iter 3/3)

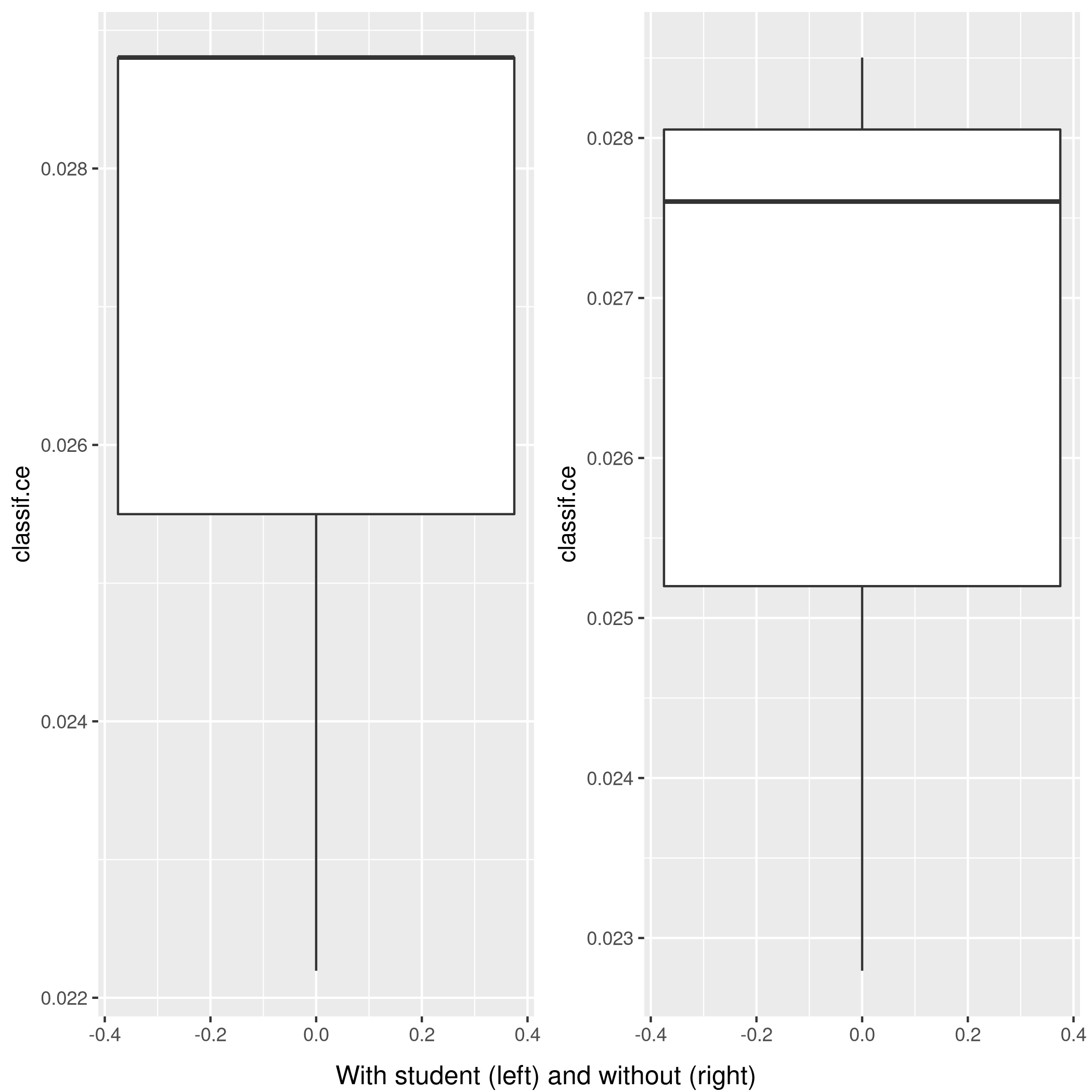

1wS<-autoplot(rr2)

2nS<-autoplot(rr)

3grid.arrange(wS,nS,ncol=2,bottom="With student (left) and without (right)")

Figure 9: Plot of accuracy

Given the results, it is fair to say that adding the student data is useful in general.

Question 5.6 - Page 199

We continue to consider the use of a logistic regression model to

predict the probability of default using income and balance on the

Default data set. In particular, we will now compute estimates for the

standard errors of the income and balance logistic regression

coefficients in two different ways: (1) using the bootstrap, and (2)

using the standard formula for computing the standard errors in the

glm() function. Do not forget to set a random seed before beginning

your analysis.

(a) Using the summary() and glm() functions, determine the

estimated standard errors for the coefficients associated with income

and balance in a multiple logistic regression model that uses both

predictors.

(b) Write a function, boot.fn() , that takes as input the Default

data set as well as an index of the observations, and that outputs the

coefficient estimates for income and balance in the multiple

logistic regression model.

(c) Use the boot() function together with your boot.fn() function

to estimate the standard errors of the logistic regression coefficients

for income and balance.

(d) Comment on the estimated standard errors obtained using the

glm() function and using your bootstrap function.

Answer

This question is slightly more specific to the packages in the book so we will use them.

a) Fit summary

1glm.fit %>% summary

1##

2## Call:

3## glm(formula = default ~ income + balance, family = binomial,

4## data = defDat, subset = trainNoCaret)

5##

6## Deviance Residuals:

7## Min 1Q Median 3Q Max

8## -2.1943 -0.1488 -0.0588 -0.0217 3.7058

9##

10## Coefficients:

11## Estimate Std. Error z value Pr(>|z|)

12## (Intercept) -1.150e+01 4.814e-01 -23.885 < 2e-16 ***

13## income 2.288e-05 5.553e-06 4.121 3.78e-05 ***

14## balance 5.593e-03 2.509e-04 22.295 < 2e-16 ***

15## ---

16## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

17##

18## (Dispersion parameter for binomial family taken to be 1)

19##

20## Null deviance: 2354.0 on 7999 degrees of freedom

21## Residual deviance: 1283.6 on 7997 degrees of freedom

22## AIC: 1289.6

23##

24## Number of Fisher Scoring iterations: 8

b) Function

1boot.fn=function(data,subs){return(coef(glm(default~income+balance,data=data, family=binomial,subset=subs)))}

1boot.fn(defDat,train_set) %>% print

1## (Intercept) income balance

2## -1.136824e+01 1.846153e-05 5.576468e-03

1glm(default~income+balance,data=defDat,family=binomial,subset=train_set) %>% summary

1##

2## Call:

3## glm(formula = default ~ income + balance, family = binomial,

4## data = defDat, subset = train_set)

5##

6## Deviance Residuals:

7## Min 1Q Median 3Q Max

8## -2.4280 -0.1465 -0.0582 -0.0218 3.7115

9##

10## Coefficients:

11## Estimate Std. Error z value Pr(>|z|)

12## (Intercept) -1.137e+01 4.813e-01 -23.618 < 2e-16 ***

13## income 1.846e-05 5.553e-06 3.324 0.000886 ***

14## balance 5.576e-03 2.529e-04 22.046 < 2e-16 ***

15## ---

16## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

17##

18## (Dispersion parameter for binomial family taken to be 1)

19##

20## Null deviance: 2313.6 on 7999 degrees of freedom

21## Residual deviance: 1266.4 on 7997 degrees of freedom

22## AIC: 1272.4

23##

24## Number of Fisher Scoring iterations: 8

We see that the statistics obtained from both are the same.

c) Bootstrap

The old fashioned way. R is the resample rate, boot.fn is the

statistic used.

1library(boot)

1##

2## Attaching package: 'boot'

1## The following object is masked from 'package:lattice':

2##

3## melanoma

1boot(defDat,boot.fn,R=184) %>% print

1##

2## ORDINARY NONPARAMETRIC BOOTSTRAP

3##

4##

5## Call:

6## boot(data = defDat, statistic = boot.fn, R = 184)

7##

8##

9## Bootstrap Statistics :

10## original bias std. error

11## t1* -1.154047e+01 -1.407368e-02 4.073453e-01

12## t2* 2.080898e-05 -6.386634e-08 4.720109e-06

13## t3* 5.647103e-03 1.350950e-05 2.111547e-04

d) Comparison

- Clearly, there is not much difference in the standard error estimates

Var | Bootstrap | Summary |

| :———: | ——— |

Intercept | 4.428026e-01 | 4.883e-01 |

income | 2.797011e-06 | 5.548e-06 |

balance | 2.423002e-04 | 2.591e-04 |

Question 5.8 - Page 200

We will now perform cross-validation on a simulated data set. (a) Generate a simulated data set as follows:

1> set . seed (1)

2> y = rnorm (100)

3> x = rnorm (100)

4> y =x -2\* x ^2+ rnorm (100)

In this data set, what is n and what is p? Write out the model used to generate the data in equation form.

(b) Create a scatterplot of \(X\) against \(Y\). Comment on what you find.

(c) Set a random seed, and then compute the LOOCV errors that result from fitting the following four models using least squares:

\(Y=\beta_0+\beta_1X+\eta\)

\(Y=\beta_0+\beta_1X+\beta_2X^2+\eta\)

\(Y=\beta_0+\beta_1X+\beta_2X^2+\beta_{3}X^{3}+\eta\)

\(Y=\beta_0+\beta_1X+\beta_2X^2+\beta_{3}X^{3}+\beta_{4}X^{4}+\eta\)

Note you may find it helpful to use the data.frame() function to

create a single data set containing both \(X\) and \(Y\).

(d) Repeat (c) using another random seed, and report your results. Are your results the same as what you got in (c)? Why?

(e) Which of the models in (c) had the smallest LOOCV error? Is this what you expected? Explain your answer.

(f) Comment on the statistical significance of the coefficient esti- mates that results from fitting each of the models in (c) using least squares. Do these results agree with the conclusions drawn based on the cross-validation results?

Answer

a) Modeling data

1set.seed(1)

2y <- rnorm(100)

3x <- rnorm(100)

4y <- x - 2*x^2 + rnorm(100)

Clearly:

- Our equation is \(y=x-2x^{2}+\epsilon\) where \(epsilon\) is normally distributed from 100 samples

- We have \(n=100\) observations

- \(p=2\) where \(p\) is the number of features

b) Visual inspection

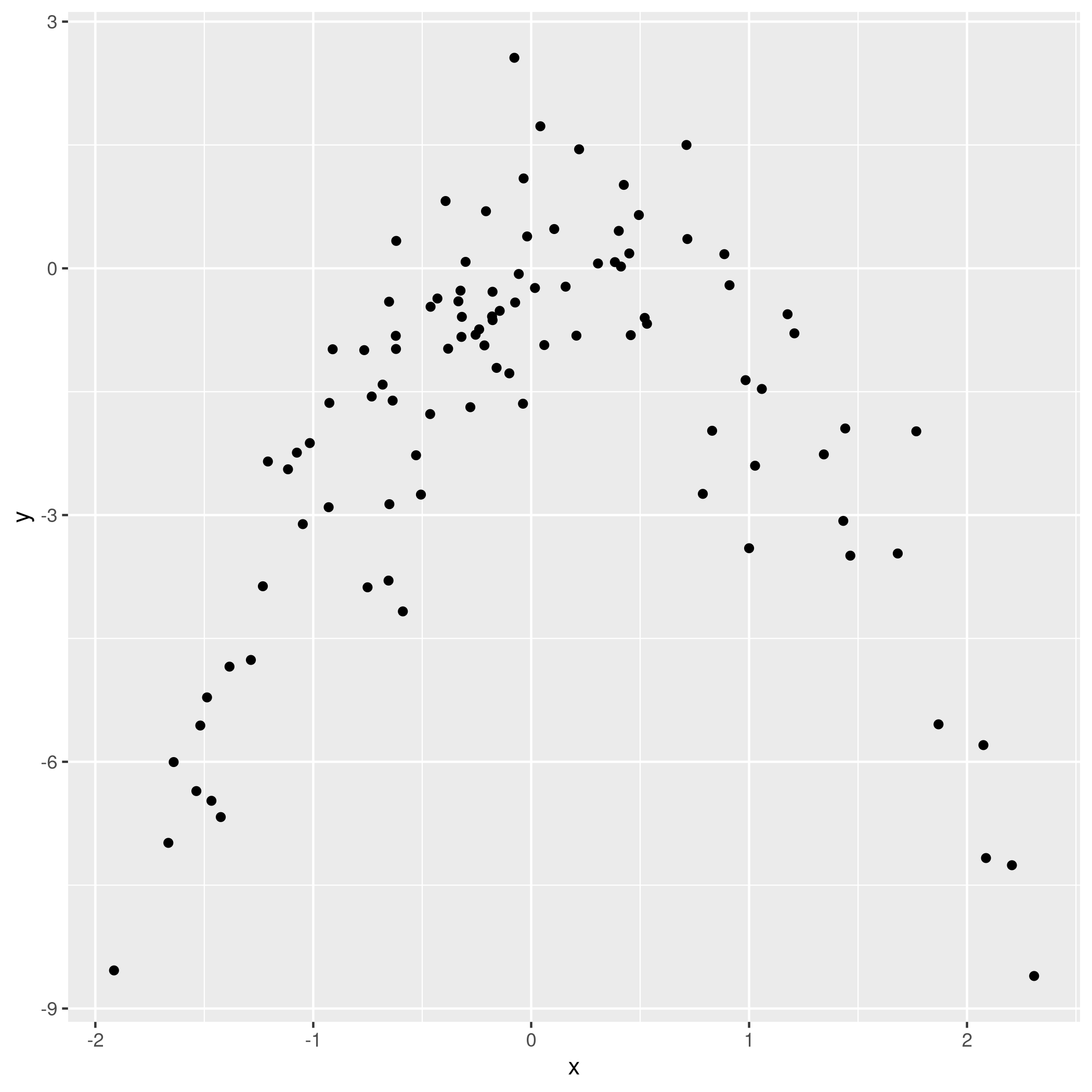

1qplot(x,y)

Figure 10: Model data plot

We observe that the data is quadratic, as we also know from the generating function, which was a quadratic equation plus normally distributed noise.

c) Least squares fits

Not very important, but here we use the caret form.

1pow=function(x,y){return(x^y)}

2dfDat <- data.frame(y,x,x2=pow(x,2),x3=pow(x,3),x4=pow(x,4))

We might have also just used poly(x,n) to skip making the data frame.

We will set our resampling method as follows:

1fitControl<-trainControl(method="LOOCV")

1train(y~x,data=dfDat,trControl=fitControl,method="lm") %>% print

1## Linear Regression

2##

3## 100 samples

4## 1 predictor

5##

6## No pre-processing

7## Resampling: Leave-One-Out Cross-Validation

8## Summary of sample sizes: 99, 99, 99, 99, 99, 99, ...

9## Resampling results:

10##

11## RMSE Rsquared MAE

12## 2.427134 0.05389864 1.878566

13##

14## Tuning parameter 'intercept' was held constant at a value of TRUE

1train(y~x+x2,data=dfDat,trControl=fitControl,method="lm") %>% print

1## Linear Regression

2##

3## 100 samples

4## 2 predictor

5##

6## No pre-processing

7## Resampling: Leave-One-Out Cross-Validation

8## Summary of sample sizes: 99, 99, 99, 99, 99, 99, ...

9## Resampling results:

10##

11## RMSE Rsquared MAE

12## 1.042399 0.8032414 0.8029942

13##

14## Tuning parameter 'intercept' was held constant at a value of TRUE

1train(y~x+x2+x3,data=dfDat,trControl=fitControl,method="lm") %>% print

1## Linear Regression

2##

3## 100 samples

4## 3 predictor

5##

6## No pre-processing

7## Resampling: Leave-One-Out Cross-Validation

8## Summary of sample sizes: 99, 99, 99, 99, 99, 99, ...

9## Resampling results:

10##

11## RMSE Rsquared MAE

12## 1.050041 0.8003517 0.8073024

13##

14## Tuning parameter 'intercept' was held constant at a value of TRUE

1train(y~x+x2+x3+x4,data=dfDat,trControl=fitControl,method="lm") %>% print

1## Linear Regression

2##

3## 100 samples

4## 4 predictor

5##

6## No pre-processing

7## Resampling: Leave-One-Out Cross-Validation

8## Summary of sample sizes: 99, 99, 99, 99, 99, 99, ...

9## Resampling results:

10##

11## RMSE Rsquared MAE

12## 1.055828 0.7982111 0.8150296

13##

14## Tuning parameter 'intercept' was held constant at a value of TRUE

d) Seeding effects

1set.seed(1995)

1train(y~x,data=dfDat,trControl=fitControl,method="lm") %>% print

1## Linear Regression

2##

3## 100 samples

4## 1 predictor

5##

6## No pre-processing

7## Resampling: Leave-One-Out Cross-Validation

8## Summary of sample sizes: 99, 99, 99, 99, 99, 99, ...

9## Resampling results:

10##

11## RMSE Rsquared MAE

12## 2.427134 0.05389864 1.878566

13##

14## Tuning parameter 'intercept' was held constant at a value of TRUE

1train(y~x+x2,data=dfDat,trControl=fitControl,method="lm") %>% print

1## Linear Regression

2##

3## 100 samples

4## 2 predictor

5##

6## No pre-processing

7## Resampling: Leave-One-Out Cross-Validation

8## Summary of sample sizes: 99, 99, 99, 99, 99, 99, ...

9## Resampling results:

10##

11## RMSE Rsquared MAE

12## 1.042399 0.8032414 0.8029942

13##

14## Tuning parameter 'intercept' was held constant at a value of TRUE

1train(y~x+x2+x3,data=dfDat,trControl=fitControl,method="lm") %>% print

1## Linear Regression

2##

3## 100 samples

4## 3 predictor

5##

6## No pre-processing

7## Resampling: Leave-One-Out Cross-Validation

8## Summary of sample sizes: 99, 99, 99, 99, 99, 99, ...

9## Resampling results:

10##

11## RMSE Rsquared MAE

12## 1.050041 0.8003517 0.8073024

13##

14## Tuning parameter 'intercept' was held constant at a value of TRUE

1train(y~x+x2+x3+x4,data=dfDat,trControl=fitControl,method="lm") %>% print

1## Linear Regression

2##

3## 100 samples

4## 4 predictor

5##

6## No pre-processing

7## Resampling: Leave-One-Out Cross-Validation

8## Summary of sample sizes: 99, 99, 99, 99, 99, 99, ...

9## Resampling results:

10##

11## RMSE Rsquared MAE

12## 1.055828 0.7982111 0.8150296

13##

14## Tuning parameter 'intercept' was held constant at a value of TRUE

We note that there is no change on varying the seed because LOOCV is exhaustive and uses n folds for each observation.

e) Analysis

1train(y~x,data=dfDat %>% subset(select=c(y,x)),trControl=fitControl,method="lm") %>% print

1## Linear Regression

2##

3## 100 samples

4## 1 predictor

5##

6## No pre-processing

7## Resampling: Leave-One-Out Cross-Validation

8## Summary of sample sizes: 99, 99, 99, 99, 99, 99, ...

9## Resampling results:

10##

11## RMSE Rsquared MAE

12## 2.427134 0.05389864 1.878566

13##

14## Tuning parameter 'intercept' was held constant at a value of TRUE

1train(y~poly(x,2),data=dfDat %>% subset(select=c(y,x)),trControl=fitControl,method="lm") %>% print

1## Linear Regression

2##

3## 100 samples

4## 1 predictor

5##

6## No pre-processing

7## Resampling: Leave-One-Out Cross-Validation

8## Summary of sample sizes: 99, 99, 99, 99, 99, 99, ...

9## Resampling results:

10##

11## RMSE Rsquared MAE

12## 1.042399 0.8032414 0.8029942

13##

14## Tuning parameter 'intercept' was held constant at a value of TRUE

1train(y~poly(x,3),data=dfDat %>% subset(select=c(y,x)),trControl=fitControl,method="lm") %>% print

1## Linear Regression

2##

3## 100 samples

4## 1 predictor

5##

6## No pre-processing

7## Resampling: Leave-One-Out Cross-Validation

8## Summary of sample sizes: 99, 99, 99, 99, 99, 99, ...

9## Resampling results:

10##

11## RMSE Rsquared MAE

12## 1.050041 0.8003517 0.8073024

13##

14## Tuning parameter 'intercept' was held constant at a value of TRUE

1train(y~poly(x,4),data=dfDat %>% subset(select=c(y,x)),trControl=fitControl,method="lm") %>% print

1## Linear Regression

2##

3## 100 samples

4## 1 predictor

5##

6## No pre-processing

7## Resampling: Leave-One-Out Cross-Validation

8## Summary of sample sizes: 99, 99, 99, 99, 99, 99, ...

9## Resampling results:

10##

11## RMSE Rsquared MAE

12## 1.055828 0.7982111 0.8150296

13##

14## Tuning parameter 'intercept' was held constant at a value of TRUE

Clearly the quadratic polynomial has the lowest error, which makes sense given how the data was generated.

f) Statistical significance

1train(y~x,data=dfDat %>% subset(select=c(y,x)),trControl=fitControl,method="lm") %>% summary %>% print

1##

2## Call:

3## lm(formula = .outcome ~ ., data = dat)

4##

5## Residuals:

6## Min 1Q Median 3Q Max

7## -7.3469 -0.9275 0.8028 1.5608 4.3974

8##

9## Coefficients:

10## Estimate Std. Error t value Pr(>|t|)

11## (Intercept) -1.8185 0.2364 -7.692 1.14e-11 ***

12## x 0.2430 0.2479 0.981 0.329

13## ---

14## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

15##

16## Residual standard error: 2.362 on 98 degrees of freedom

17## Multiple R-squared: 0.009717, Adjusted R-squared: -0.0003881

18## F-statistic: 0.9616 on 1 and 98 DF, p-value: 0.3292

1train(y~poly(x,2),data=dfDat %>% subset(select=c(y,x)),trControl=fitControl,method="lm") %>% summary %>% print

1##

2## Call:

3## lm(formula = .outcome ~ ., data = dat)

4##

5## Residuals:

6## Min 1Q Median 3Q Max

7## -2.89884 -0.53765 0.04135 0.61490 2.73607

8##

9## Coefficients:

10## Estimate Std. Error t value Pr(>|t|)

11## (Intercept) -1.8277 0.1032 -17.704 <2e-16 ***

12## `poly(x, 2)1` 2.3164 1.0324 2.244 0.0271 *

13## `poly(x, 2)2` -21.0586 1.0324 -20.399 <2e-16 ***

14## ---

15## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

16##

17## Residual standard error: 1.032 on 97 degrees of freedom

18## Multiple R-squared: 0.8128, Adjusted R-squared: 0.8089

19## F-statistic: 210.6 on 2 and 97 DF, p-value: < 2.2e-16

1train(y~poly(x,3),data=dfDat %>% subset(select=c(y,x)),trControl=fitControl,method="lm") %>% summary %>% print

1##

2## Call:

3## lm(formula = .outcome ~ ., data = dat)

4##

5## Residuals:

6## Min 1Q Median 3Q Max

7## -2.87250 -0.53881 0.02862 0.59383 2.74350

8##

9## Coefficients:

10## Estimate Std. Error t value Pr(>|t|)

11## (Intercept) -1.8277 0.1037 -17.621 <2e-16 ***

12## `poly(x, 3)1` 2.3164 1.0372 2.233 0.0279 *

13## `poly(x, 3)2` -21.0586 1.0372 -20.302 <2e-16 ***

14## `poly(x, 3)3` -0.3048 1.0372 -0.294 0.7695

15## ---

16## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

17##

18## Residual standard error: 1.037 on 96 degrees of freedom

19## Multiple R-squared: 0.813, Adjusted R-squared: 0.8071

20## F-statistic: 139.1 on 3 and 96 DF, p-value: < 2.2e-16

1train(y~poly(x,4),data=dfDat %>% subset(select=c(y,x)),trControl=fitControl,method="lm") %>% summary %>% print

1##

2## Call:

3## lm(formula = .outcome ~ ., data = dat)

4##

5## Residuals:

6## Min 1Q Median 3Q Max

7## -2.8914 -0.5244 0.0749 0.5932 2.7796

8##

9## Coefficients:

10## Estimate Std. Error t value Pr(>|t|)

11## (Intercept) -1.8277 0.1041 -17.549 <2e-16 ***

12## `poly(x, 4)1` 2.3164 1.0415 2.224 0.0285 *

13## `poly(x, 4)2` -21.0586 1.0415 -20.220 <2e-16 ***

14## `poly(x, 4)3` -0.3048 1.0415 -0.293 0.7704

15## `poly(x, 4)4` -0.4926 1.0415 -0.473 0.6373

16## ---

17## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

18##

19## Residual standard error: 1.041 on 95 degrees of freedom

20## Multiple R-squared: 0.8134, Adjusted R-squared: 0.8055

21## F-statistic: 103.5 on 4 and 95 DF, p-value: < 2.2e-16

- Clearly, the second order terms are the most significant, as expected

Question 5.9 - Page 201

We will now consider the Boston housing data set, from the MASS library.

(a) Based on this data set, provide an estimate for the population

mean of medv. Call this estimate \(\hat{\mu}\).

(b) Provide an estimate of the standard error of \(\hat{\mu}\). Interpret this result. Hint: We can compute the standard error of the sample mean by dividing the sample standard deviation by the square root of the number of observations.

(c) Now estimate the standard error of \(\hat{\mu}\) using the bootstrap. How does this compare to your answer from (b)?

(d) Based on your bootstrap estimate from (c), provide a 95 %

confidence interval for the mean of medv. Compare it to the results

obtained using t.test(Boston\$medv). Hint: You can approximate a 95 %

confidence interval using the formula

\([\hat{\mu} − 2SE(\hat{\mu}), \hat{\mu} + 2SE(\hat{\mu})]\).

(e) Based on this data set, provide an estimate, \(\hat{\mu_{med}}\),

for the median value of medv in the population.

(f) We now would like to estimate the standard error of \(\hat{\mu}\) med. Unfortunately, there is no simple formula for computing the standard error of the median. Instead, estimate the standard error of the median using the bootstrap. Comment on your findings.

(g) Based on this data set, provide an estimate for the tenth

percentile of medv in Boston suburbs. Call this quantity

\(\hat{\mu_{0.1}}\). (You can use the quantile() function.)

(h) Use the bootstrap to estimate the standard error of \(\hat{\mu_{0.1}}\). Comment on your findings.

Answer

1boston<-MASS::Boston

- Reminder

1boston %>% summary %>% print

1## crim zn indus chas

2## Min. : 0.00632 Min. : 0.00 Min. : 0.46 Min. :0.00000

3## 1st Qu.: 0.08204 1st Qu.: 0.00 1st Qu.: 5.19 1st Qu.:0.00000

4## Median : 0.25651 Median : 0.00 Median : 9.69 Median :0.00000

5## Mean : 3.61352 Mean : 11.36 Mean :11.14 Mean :0.06917

6## 3rd Qu.: 3.67708 3rd Qu.: 12.50 3rd Qu.:18.10 3rd Qu.:0.00000

7## Max. :88.97620 Max. :100.00 Max. :27.74 Max. :1.00000

8## nox rm age dis

9## Min. :0.3850 Min. :3.561 Min. : 2.90 Min. : 1.130

10## 1st Qu.:0.4490 1st Qu.:5.886 1st Qu.: 45.02 1st Qu.: 2.100

11## Median :0.5380 Median :6.208 Median : 77.50 Median : 3.207

12## Mean :0.5547 Mean :6.285 Mean : 68.57 Mean : 3.795

13## 3rd Qu.:0.6240 3rd Qu.:6.623 3rd Qu.: 94.08 3rd Qu.: 5.188

14## Max. :0.8710 Max. :8.780 Max. :100.00 Max. :12.127

15## rad tax ptratio black

16## Min. : 1.000 Min. :187.0 Min. :12.60 Min. : 0.32

17## 1st Qu.: 4.000 1st Qu.:279.0 1st Qu.:17.40 1st Qu.:375.38

18## Median : 5.000 Median :330.0 Median :19.05 Median :391.44

19## Mean : 9.549 Mean :408.2 Mean :18.46 Mean :356.67

20## 3rd Qu.:24.000 3rd Qu.:666.0 3rd Qu.:20.20 3rd Qu.:396.23

21## Max. :24.000 Max. :711.0 Max. :22.00 Max. :396.90

22## lstat medv

23## Min. : 1.73 Min. : 5.00

24## 1st Qu.: 6.95 1st Qu.:17.02

25## Median :11.36 Median :21.20

26## Mean :12.65 Mean :22.53

27## 3rd Qu.:16.95 3rd Qu.:25.00

28## Max. :37.97 Max. :50.00

1boston %>% str %>% print

1## 'data.frame': 506 obs. of 14 variables:

2## $ crim : num 0.00632 0.02731 0.02729 0.03237 0.06905 ...

3## $ zn : num 18 0 0 0 0 0 12.5 12.5 12.5 12.5 ...

4## $ indus : num 2.31 7.07 7.07 2.18 2.18 2.18 7.87 7.87 7.87 7.87 ...

5## $ chas : int 0 0 0 0 0 0 0 0 0 0 ...

6## $ nox : num 0.538 0.469 0.469 0.458 0.458 0.458 0.524 0.524 0.524 0.524 ...

7## $ rm : num 6.58 6.42 7.18 7 7.15 ...

8## $ age : num 65.2 78.9 61.1 45.8 54.2 58.7 66.6 96.1 100 85.9 ...

9## $ dis : num 4.09 4.97 4.97 6.06 6.06 ...

10## $ rad : int 1 2 2 3 3 3 5 5 5 5 ...

11## $ tax : num 296 242 242 222 222 222 311 311 311 311 ...

12## $ ptratio: num 15.3 17.8 17.8 18.7 18.7 18.7 15.2 15.2 15.2 15.2 ...

13## $ black : num 397 397 393 395 397 ...

14## $ lstat : num 4.98 9.14 4.03 2.94 5.33 ...

15## $ medv : num 24 21.6 34.7 33.4 36.2 28.7 22.9 27.1 16.5 18.9 ...

16## NULL

a) Mean

1muhat=boston$medv %>% mean()

2print(muhat)

1## [1] 22.53281

b) Standard error

Recall that \(SE=\frac{SD}{\sqrt{N_{obs}}}\)

1boston$medv %>% sd/(nrow(boston)^0.5) %>% print

1## [1] 22.49444

1## [1] 0.4088611

c) Bootstrap estimate

1library(boot)

2myMean<-function(frame,ind){return(mean(frame[ind]))}

1boot(boston$medv,myMean,R=184) %>% print

1##

2## ORDINARY NONPARAMETRIC BOOTSTRAP

3##

4##

5## Call:

6## boot(data = boston$medv, statistic = myMean, R = 184)

7##

8##

9## Bootstrap Statistics :

10## original bias std. error

11## t1* 22.53281 0.03451839 0.409621

We see that the bootstrapped error over 184 samples is 0.4341499 while

without it we had 0.4088611 which is similar enough.

d) Confidence intervals with bootstrap and t.test

1boston$medv %>% t.test %>% print

1##

2## One Sample t-test

3##

4## data: .

5## t = 55.111, df = 505, p-value < 2.2e-16

6## alternative hypothesis: true mean is not equal to 0

7## 95 percent confidence interval:

8## 21.72953 23.33608

9## sample estimates:

10## mean of x

11## 22.53281

We can approximate this with what we already have

1bRes=boot(boston$medv,myMean,R=184)

2seBoot<-bRes$t %>% var %>% sqrt

3xlow=muhat-2*(seBoot)

4xhigh=muhat+2*(seBoot)

5c(xlow,xhigh) %>% print

1## [1] 21.72675 23.33887

Our intervals are also pretty close to each other.

e) Median

1boston$medv %>% sort %>% median %>% print

1## [1] 21.2

f) Median standard error

We can reuse the logic of the myMean function defined previously.

1myMedian=function(data,ind){return(median(data[ind]))}

1boston$medv %>% boot(myMedian,R=1500) %>% print

1##

2## ORDINARY NONPARAMETRIC BOOTSTRAP

3##

4##

5## Call:

6## boot(data = ., statistic = myMedian, R = 1500)

7##

8##

9## Bootstrap Statistics :

10## original bias std. error

11## t1* 21.2 -0.03773333 0.387315

We see that the standard error is 0.3767072.

g) Tenth percentile

1mu0one<-boston$medv %>% quantile(c(0.1))

2print(mu0one)

1## 10%

2## 12.75

h) Bootstrap

Once again.

1myQuant=function(data,ind){return(quantile(data[ind],0.1))}

1boston$medv %>% boot(myQuant,R=500) %>% print

1##

2## ORDINARY NONPARAMETRIC BOOTSTRAP

3##

4##

5## Call:

6## boot(data = ., statistic = myQuant, R = 500)

7##

8##

9## Bootstrap Statistics :

10## original bias std. error

11## t1* 12.75 -0.0095 0.4951415

The standard error is 0.5024526

James, G., Witten, D., Hastie, T., & Tibshirani, R. (2013). An Introduction to Statistical Learning: with Applications in R. Berlin, Germany: Springer Science & Business Media. ↩︎

Lang et al., (2019). mlr3: A modern object-oriented machine learning framework in R. Journal of Open Source Software, 4(44), 1903, https://doi.org/10.21105/joss.01903 ↩︎

![]()